program design")

7 tips for effective health savings account (HSA) program design

Some employees may not be saving adequately for retirement, but one potential resource is already included in the benefits offerings of many organizations: Health Savings Accounts (HSAs). Our new Voya Perspectives Orange Paper reveals how employers can amplify the power of HSAs — to help bridge the health-wealth savings gap and encourage improved employee financial outcomes.

Factors that may affect American workers’ ability to save for the future include inflation and ever-increasing health care costs — which tend to increase with age. According to the Employee Benefit Research Institute (EBRI), a man will need $166,000 in savings and a woman will need $197,000 in order to have a 90% chance of meeting health care spending needs throughout retirement. But defined contribution retirement plan balances for some people fall short of these numbers, creating a gap in retirement health care savings.

How can employers help their employees prepare for retirement and save enough money throughout their careers? One answer could lie in an already-popular benefit offering: HSAs.

Living for today, preparing for tomorrow

HSAs can help employees strike a balance between living today and preparing for tomorrow. These triple tax-advantaged accounts allow the employee to contribute pre-tax funds that can be used tax-free for eligible health care costs throughout their life, as long as there are funds in the account. Once the account is opened, it does not expire — regardless of employment status. And as long as the funds in the account are used for qualified health care expenses, there are no penalties or taxes.

Plus, HSAs are beneficial for the employers that offer them. Here are just a few examples for employers to consider around savings opportunities when including an HSA option in their benefits package. High-Deductible Health Plans (HDHPs), which are required for individuals wishing to contribute to an HSA, have an opportunity to be more cost-effective for employers than other health insurance plan types. Employers’ HSA contributions are not subject to some payroll taxes. This may vary by state.

So where to begin? Below are several best practices to consider for creating a successful HSA program, which can encourage optimal financial outcomes for employees and employers alike.

7 tips to design an effective HSA program

Just like designing a retirement program, employers should use care and attention-to-detail to create a multi-year strategy that increases employee participation in HSAs. Here are Voya’s top tips to consider:

1. Choose a long-term HSA administrator

Since HSAs are adjacent to health insurance plans, many organizations end up using the same medical carrier for both. However, doing this may create disruptions further down the line.

If the organization ever decides to make a change in insurance carrier, they would also need to make changes their HSA offering. This means new cards, new logins and possibly new fees. Plus, employees may lose access to their funds while the switch is made.

2. Provide a diversified investment menu

Since HSA funds can potentially sit for a long time, employees may be interested in the potential of growing their contributions. To do this, employers may wish to consider providing a way to invest pre-tax HSA funds once their balance reaches a certain threshold.

As employers are establishing or updating their organization’s HSA solution, it’s important to ensure their provider can offer a full array of investment options. And be sure to communicate there are risks with any investment — account holders should make sure to fully explore those risks before choosing to invest their balance.

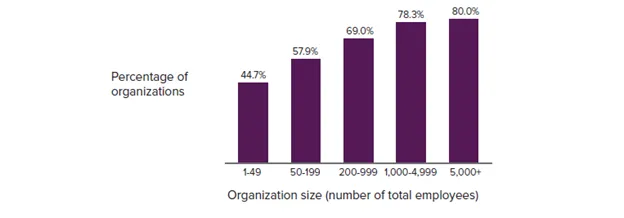

Percentage of organizations that offer investment options for HSA contributions

3. Ensure fees are reasonable and transparent

Transparency about HSA investment capabilities and fees is key. As with retirement plans, high fees on underlying investments along with administrative fees can eat into growth potential. Reasonable fees that are explained clearly may encourage employees to invest for long-term growth rather than simply parking their HSA assets in a cash account.

4. Use smart spending technology

It’s possible for employees to have multiple health spending accounts like Dependent Care Flexible Spending Accounts (FSAs), Limited Purpose FSAs and HSAs. When that happens, paying for their own or their families’ health care can become a complex equation.

Employers can lessen this confusion by providing smart spending technology. In other words, make their debit card do the work for them across their accounts.

How smart spending tech works:

An employee has a Limited Purpose FSA and an HSA. They use a smart debit card to pay for a qualified dental expense. The card automatically pulls from the Limited Purpose FSA balance first and saves the HSA funds for the future.

5. Consider contributing

Employers can consider contributing to HSAs to encourage participation, similar to how they handle retirement plan contributions. For example, employers can provide a flat HSA contribution (e.g., $300 a year), providing employees with funds to pay out-of-pocket medical expenses early in the year, before the employee contributions have accumulated.3

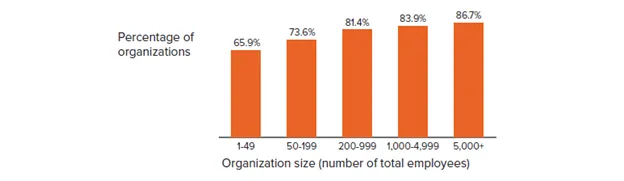

Percentage of organizations that contribute to the HSA

6. Create default elections

By creating a default election for employees enrolled in an HSA-compatible HDHP, employers can help them build meaningful balances without needing to take direct action.

The Voya Behavioral Finance Institute for Innovation conducted research to determine a range of default contribution percentages that do not affect opt-outs — identifying 3% to 10% as the sweet spot. Note: Employers should consult legal counsel to ensure that any planned defaults do not trigger ERISA provisions.

7. Set goals and track them

Just as employers take great care to measure and track many aspects of their retirement plans, they should do the same for HSAs. Employers can set targets for program metrics. If goals come up short, they can respond by defining action steps to improve.

Get help with program design and administration

Employers can collaborate with intermediaries (such as benefits brokers, financial professionals and consultants) to implement programs that serve diverse employee populations. They can dedicate more time and attention to the details than many organizations’ HR departments can do on their own. Plus, having an experienced and knowledgeable administrator is never a bad idea.

Intermediaries can make employers’ jobs easier by:

- Providing benefits solutions that simplify administration for employers

- Offering insights and experiences that ease decision-making for employees

- Assisting with HSA program design that seamlessly integrates into the employer’s full benefits package

- Choosing an HSA provider that can minimize potential disruption for employees if a health-insurer change is warranted later

- Developing a year-round HSA employee communication and education strategy that helps employees understand the full potential of their retirement plan and HSA

HSA-focused education is essential to success

When open enrollment comes around annually, employees are faced with a big task: choosing the benefits they’ll need next year from a laundry list of options. It’s no surprise that they may not fully understand the advantages and disadvantages of each employer-sponsored benefit or account available to them.

By creating a communication strategy that concentrates on financial wellness, dispelling HSA myths and seeing “the bigger picture,” organizations can motivate employees to learn more about HSAs as an effective health savings account; one that can be used on eligible medical expenses today but also offers the potential to improve their retirement readiness.

Again, intermediaries can offer specialized knowledge when it comes to designing, communicating and facilitating benefits.

About Voya and our Orange Papers

As a workplace benefits and savings provider, Voya knows the dynamics that surround people’s health plans and financial accounts. We aspire to clear the path to financial confidence for more fulfilling lives, so we thoughtfully design our products and services, including our HSAs, to be easy and engaging for employees.

Part of this vision is to better understand how providers, intermediaries and employers can help individuals improve their financial outcomes. Our Voya Perspectives Orange Papers share our research findings and recommendations for industry-wide innovations.

Text representation of article graphics (for screen reader accessibility):

Graphic 1: Percentage of organizations that offer investment options for HSA contributions

| Percentage of organizations | Organization size (number of total employees) |

| 44.7% | 1-49 |

| 57.9% | 50-199 |

| 69.0% | 200-999 |

| 78.3% | 1,000-4,999 |

| 80.0% | 5,000+ |

Graphic 2: Percentage of organizations that contribute to the HSA

| Percentage of organizations | Organization size (number of total employees) |

| 65.9% | 1-49 |

| 73.6% | 50-199 |

| 81.4% | 200-999 |

| 83.9% | 1,000-4,999 |

| 86.7% | 5,000+ |

{kind=link}